Europe connected car industry outlook from 2024 to 2034

Europe Connected Car Industry Outlook from 2024 to 2034

Press Release

According to Future Market Insights Europe connected car market is evaluated to be USD 15 billion in 2024. The industry is expected to reach USD 65.3 billion by 2034. The industry is projected to register a 15.8% CAGR from 2024 to 2034.

The demand for electric cars in Europe is increasing at a rapid pace. According to the European Automobile Manufacturers’ Association (ACEA), around 139,702 battery-electric car units were registered in the European Union (EU) in September 2024. Electric car buyers opt for sustainable and technologically advanced options, which are expected to improve sales.

The industry goes from strength to strength with the advent of new technology. One such technology that is making waves is 5G. Customers are accustomed to 5G technology through their smartphones and are looking for cars that replicate it. Manufacturers are thus ensuring their cars remain up-to-date and have fast connection speeds with the integration of 5G technology.

Connected cars allow for seamless integration of IoT, AI, autonomous driving, and other features. Customers are enthralled by features like automatic parking and virtual reality displays. Connected cars allow for the smooth functioning of these technologies and are thus seeing high demand in Europe.

Europe Connected Car Industry Assessment

| Attributes | Description |

|---|---|

| Estimated Europe Connected Car Industry Size (2024E) | USD 15 billion |

| Projected Europe Connected Car Industry Value (2034F) | USD 65.3 billion |

| Value-based CAGR (2024 to 2034) | 15.8% |

Semi-annual Industry Update

The Europe connected car industry has evident growth possibilities. The expansion of the sector is predicted to vary from 2024 up to 2034. The first half of 2023 to 2033 is expected to experience a CAGR of 14.4%. For the second half, the demand is expected to register a CAGR of 15%.

| Particular | Value CAGR |

|---|---|

| H1 | 14.4% (2023 to 2033) |

| H2 | 15% (2023 to 2033) |

| H1 | 15.1% (2024 to 2034) |

| H2 | 16.3% (2024 to 2034) |

In the 2024 to 2034 period, the first half remains at a steady CAGR of 15.1%. The latter half of the period from 2024 to 2034, however, registers a higher CAGR of 16.3 %.

Key Industry Highlights

Revving Up the Future: How Car Manufacturers are Shifting Transportation to In-Car Entertainment

The static function of cars as a moving vehicle is falling by the wayside. In Europe, what a car does when not on the road is gaining immense traction. Manufacturers are paying more attention to the smart entertainment system provided in cars. In-car streaming and mobile-like interfaces are becoming common features in European cars.

Moreover, these electric cars are being promoted as a vehicle with entertainment. Increasing popularity of carpool karaoke, especially in Western countries, is helping these manufacturers position their cars among consumers. This is improving their visibility and brand recognition.

At the same time, infotainment is also assisting drivers. With the help of personal assistants like Alexa and remote control features, drivers are being assisted in their journeys. By integrating state-of-the-art infotainment systems, connected car manufacturers have the opportunity to cross new horizons in terms of demand.

Favorable Regulations Drives Industry Forward in Europe

The progress of connected cars in Europe is accelerating in Europe with favorable laws being put into practice. For instance, the Data Act, introduced by the EU in 2022. The act has made it easier for data to be shared, including data collected by connected cars. The EU has also laid out the framework for the approval of driverless and automated vehicles. Hence, regulations have laid the path to progress for connected cars in the region.

Concerns Regarding Data Privacy Act as Roadblock on the Development Path

While customers are enamored of the connectivity in cars, a significant subset of them is also worried about data privacy. End users are hesitant about sharing driving data with companies and are thus reluctant to buy connected cars. Consumers are also wary of the threat of hackers and other problems regarding cyber security. Thus, the threat of data breaches slows down the growth rate.

2019 to 2023 Europe Connected Car Sales Analysis Compared to Demand Forecast from 2024 to 2034

In 2019, the industry value was USD 7.8 billion. By 2023, the value had grown to USD 13.1 billion, registering growth at a CAGR of 13.7%.

Supply chain disruptions caused by the pandemic affected the whole automotive sector and the Europe connected car industry was no different. According to the ACEA, sales of cars plunged by almost 32% in the first two quarters of 2020. The connected cars segment was also duly affected.

However, the industry was bolstered by the constant introduction of new technology. With more cars being equipped with 5G connectivity, these cars provided a thoroughly modern experience to customers. Advances in remote control, driverless vehicles, and other areas also turned heads and kept connected cars in the public eye.

Industry Concentration

Tier 1 companies like Continental AG and Robert Bosch GmbH have carved out a significant portion of the Europe industry share. These companies focus on equipping their cars with cutting-edge technology. Partnerships with tech giants are also focused upon to bring out innovations. For instance, Harman Corporation collaborated with Amazon in May 2022 to develop safe connected vehicles. In 2024, the revenue share of tier 1 companies is expected to be a dominant 71%.

Tier 2 companies have established a niche for themselves by making available satellite navigation devices in cars. The focus of these organizations is on providing real-time accurate data to drivers. The accurate map locating services provided by these companies also aid connected cars with autonomous driving. The revenue share of tier 2 companies is estimated to be 33% in 2024.

Get the data you need at a Fraction of the cost

Personalize your report by choosing insights you need

and save 40%!Share Specifics with Me

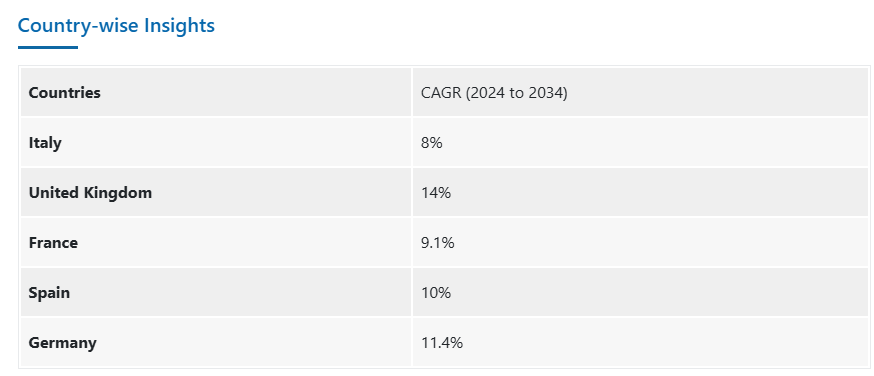

Technological Advancements and Investments to Shape Germany’s Connected Car Market

The industry in Germany is expected to register a CAGR of 11.4% over the period from 2024 to 2034. The Germany automobile sector is characterized by its technological advancement. Hence, there is significant scope for connected cars in the country.

The technological advancements in the industry are also being boosted by investment influx. For instance, DC Connected Car GmbH secured more than USD 2 billion in seed funding in August 2024. The enterprise specializes in AI-driven solutions.

Government Encouragement Drives Industry in the United Kingdom

The United Kingdom connected car industry is anticipated to advance at a CAGR of 14% over the forecast period. The prospects of the industry in the United Kingdom are being bolstered by government support. For instance, the government created the Connected and Automated Mobility (CAM) Scale-Up UK Programme in 2020.

The aim of the scheme is to support small and medium-scale organizations in furthering their research regarding autonomous vehicles. In the first four years of its existence, the initiative supported over 20 businesses in the autonomous vehicle sector.

Category-wise Insights

Vehicle-to-infrastructure (V2I) connectivity is prioritized in Europe. The desire for fast speeds sees Europeans lean towards 4G connectivity.

Avoiding Traffic Congestion and Improving Road Safety See Customers Veer Towards V2I Communication

| Segment | Vehicle-to-infrastructure (V2I) (Communication Type) |

|---|---|

| Value Share (2024) | 38% |

Vehicle-to-infrastructure (V2I) communication is expected to account for 38% of the industry share in 2024. Customers are becoming more aware of the impact of V2I technology in solving problems on the road. V2I technology helps with reducing traffic congestion and enhancing road safety. Customers save precious time by communicating with road infrastructure such as RFID readers and cameras. Knowledge is obtained about roadblocks, diversions, closures, and more, ensuring a smoother ride.

Need for Fast Speed Sees 4G Rise to the Top of the Connectivity Technology Segment

| Segment | 4G LTE (Connectivity Technology) |

|---|---|

| Value Share (2024) | 44% |

4G LTE is anticipated to hold 44% of the industry share in 2024. Customers are drawn to the latest connectivity technology and 4G has proven trustworthy. However, with the advent of 5G, and the impending launch of 6G, 4G’s status at the top is time barred. For the moment though, 4G LTE remains the top choice in connected cars.

Competition Outlook

The industry is fairly fragmented, with no player having established dominance in Europe. In line with the fast-moving nature of the industry, companies are concentrating on keeping the product line moving. For this purpose they are establishing partnerships with tech giants, for instance, Robert Bosch with Microsoft. Acquisitions are also common, as evidenced by HARMAN International acquiring Savari Inc. in 2021.

Industry Updates

- In May 2024, Dutch organization KPN IoT and Austrian connectivity provider Freeway collaborated to launch a monetization platform. The platform makes it easier for users to generate revenue streams from their connected cars in Europe.

- In April 2024, Hyundai Motor Europe established Hyundai Connected Mobility. The division aims to enhance the customer experience in Europe regarding smart mobility solutions and software-controlled cars.

Leading Europe Connected Car Manufacturers

- Robert Bosch GmbH

- HARMAN International

- Visteon Corporation

- Continental AG

- Audi AG

- BMW Group

- Autoliv Inc.

- Delphi Automotive LLP

- Daimler AG

- Verizon Communication

- Denso Corporation

Key Segments of Industry Report

By Communication Type:

The communication type segment includes Vehicle-to-Vehicle (V2V), Vehicle-to-Infrastructure (V2I), Vehicle-To-Pedestrian (V2P), and others.

By Application:

Driver assistance, infotainment, vehicle safety & security, telematics & navigation, and other applications are categorized in this segment.

By Connectivity Technology:

Based on the connectivity technology, the industry is divided into 3G, 4G LTE, 5G, and others.

By Vehicle Type:

Based on the vehicle type, the industry is bifurcated into passenger cars and commercial vehicles.

By End User:

Based on the end user, the industry is bifurcated into automotive OEMs and automotive aftermarket.

By Country:

United Kingdom, Germany, France, Spain, Italy, BENELUX, Russia, and the rest of Europe are covered in the report.