Global usage based insurance market size, share, trends and forecast 2024-2033

Global Usage-based Insurance Market Size, Share, Trends Analysis Report By Type (Pay-As-You-Drive (PAYD), Pay-How-You-Drive (PHYD), Manage-How-You-Drive (MHYD)), By Technology (OBD-II-Based UBI, Smartphone-Based UBI, Embedded Telematics-Based UBI, Other Technologies), By Vehicle Type (Passenger Vehicles, Commercial Vehicles), Region and Companies – Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2024-2033

Press Release, 4th November 2024

Report Overview

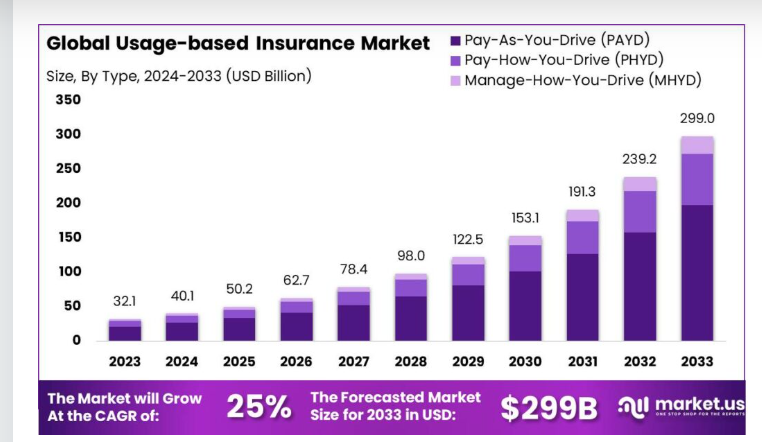

The Global Usage-based Insurance Market size is expected to be worth around USD 299 Billion By 2033, from USD 32.1 Billion in 2023, growing at a CAGR of 25.5% during the forecast period from 2024 to 2033. In 2023, North America held a dominant market position, capturing more than a 40.5% share, holding USD 13 Billion revenue.

Usage-Based Insurance (UBI) is a type of auto insurance that tailors pricing based on the actual behavior of drivers, using telematics technology to monitor vehicle use. This approach allows insurers to offer premiums that reflect individual driving habits, rewarding safe driving with lower costs and aligning risk assessment more closely with actual driver behavior.

The usage-based insurance market is growing rapidly as more consumers and insurers recognize the benefits of technology-driven policies. With advancements in IoT and mobile technologies, insurers are better equipped to collect accurate driving data, making UBI more accessible and appealing to a broader audience. This market is expanding not only in traditional automotive insurance but also in emerging sectors such as shared mobility and autonomous vehicles, which promise new opportunities for UBI applications.

Key drivers of the UBI market include the growing penetration of telematics and connected vehicle technologies, which enable the real-time tracking of driving behaviors like speed, location, and overall vehicle usage. The automotive industry’s expansion and increasing vehicle ownership rates contribute to this rise, alongside technological advancements that improve the accuracy and ease of data collection and analysis.

Technological developments are central to the expansion of the UBI market. Innovations in smartphone applications, along with integrated vehicle telematics systems, are crucial. These technologies not only facilitate the widespread adoption of UBI by lowering costs but also enhance the accuracy and reliability of data collected, which is vital for tailoring insurance premiums accurately based on user behavior.

For instance, In August 2023, Citroen launched a Usage-Based Insurance (UBI) program specifically for its electric vehicle, the eC3, in partnership with ICICI Lombard General Insurance. This innovative offering aims to redefine how insurance is structured for EV owners by linking premiums to driving behavior. It represents a forward-thinking approach, rewarding drivers for safe driving habits while encouraging a more responsible driving culture among eC3 users.

Demand for UBI is fueled by its potential to reduce insurance costs for safe drivers, offer more accurate pricing, and improve customer engagement through personalized insurance policies. As vehicles become more connected, the ease of integrating UBI with existing automotive technologies has also enhanced market adoption.

The UBI market is ripe with opportunities, particularly in developing personalized insurance products that can adapt to individual driving patterns. There is also potential for growth in regions with high vehicle sales and increasing adoption of connected car technologies. Moreover, ongoing innovations in mobile and communication technologies are likely to create new avenues for deploying UBI at a lower cost and on a larger scale.

According to the findings of IMS Tech, out of roughly 875 million automotive insurance policies, around 20 million are usage-based. This highlights a growing interest in usage-based insurance (UBI) as drivers seek more flexible and personalized insurance solutions.

In recent years, the mobile UBI segment has also expanded, with approximately 4.8 million policyholders adopting mobile telematics solutions. These solutions allow insurers to collect real-time driving data, making premiums more reflective of individual driving habits. This trend reflects a shift toward data-driven insurance models, which offer potential cost savings for both insurers and policyholders.

Surveys in the UK suggest that about 70% of drivers anticipate covering more miles in 2023 than in the previous year, signaling an increase in road travel. Consequently, around 58% of UK drivers express a preference for telematics-based insurance to help manage the higher costs associated with this increased mileage.

Key Takeaways

- The Global Usage-Based Insurance (UBI) Market is projected to experience substantial growth, anticipated to reach USD 299 Billion by 2033, up from USD 32.1 Billion in 2023. This represents an impressive Compound Annual Growth Rate (CAGR) of 25.5% over the forecast period from 2024 to 2033.

- In 2023, North America emerged as the leading region in the UBI market, capturing a significant 40.5% share, equivalent to USD 13 Billion in revenue. This dominance reflects the region’s rapid adoption of telematics and increasing consumer demand for personalized insurance solutions.

- The Pay-As-You-Drive (PAYD) model led the market in 2023, accounting for more than 66.4% of the UBI industry share. This segment’s popularity is driven by its flexibility and cost-saving potential for consumers, especially for low-mileage drivers.

- Additionally, the OBD-II-Based UBI segment held a prominent position, capturing 45.1% of the market share in 2023. This dominance highlights the widespread use of onboard diagnostics (OBD-II) systems in telematics-enabled vehicles, providing insurers with essential driving data.

- Finally, the Passenger Vehicles segment dominated the UBI market with a 67% share in 2023. This reflects the growing trend of using telematics-based insurance for private vehicle owners, who seek premiums that align closely with their driving behaviors.

Type Analysis

In 2023, the Pay-As-You-Drive (PAYD) segment held a dominant market position in the Usage-Based Insurance (UBI) industry, capturing more than a 66.4% share. This substantial market share can be attributed to the direct correlation between insurance costs and actual vehicle usage, which appeals to a broad consumer base.

PAYD models are particularly popular among drivers who use their vehicles infrequently as they offer a cost-effective alternative to traditional flat-rate insurance policies. By charging premiums based on the distance driven, insurers can attract customers looking for financial flexibility and fairness.

The dominance of PAYD is also reinforced by the growing consumer preference for digital and mobile platforms that support real-time data tracking and sharing. Technological advancements have made it easier and more cost-effective for insurers to implement PAYD systems. These systems utilize telematics devices installed in vehicles or mobile apps that monitor driving distance and, in some cases, driving behaviors.

The ease of integration with existing technologies encourages both insurers and consumers to favor PAYD over other types. Furthermore, regulatory support for PAYD programs in various regions has bolstered their adoption. Governments are increasingly recognizing the potential of PAYD to encourage safer driving habits and reduce vehicle emissions by incentivizing drivers to drive less. This regulatory encouragement, combined with the economic benefits for consumers, positions PAYD as a leading segment in the UBI market.

Technology Analysis

In 2023, the OBD-II-Based UBI segment held a dominant market position, capturing more than a 45.1% share of the Usage-Based Insurance (UBI) market. This segment’s leadership stems primarily from the established reliability and accuracy of OBD-II devices in collecting vehicle data.

These devices, which plug directly into a vehicle’s onboard diagnostics system, provide insurers with precise information on driving patterns, vehicle health, and compliance with safety standards. This level of detail allows for more accurately tailored insurance premiums, which can be adjusted based on individual risk assessments.

The prevalence of OBD-II technology in vehicles, particularly in markets with high regulatory standards like the United States and the European Union, has facilitated its adoption. Most vehicles manufactured since the mid-1990s are equipped with an OBD-II port, making the integration of UBI programs straightforward for insurers without requiring significant additional investment from consumers.

This ease of integration, coupled with the minimal effort required from policyholders to participate, enhances the attractiveness of OBD-II-Based UBI programs. Moreover, the data security features inherent in OBD-II devices give them an edge over other technologies. Since these devices connect directly to the vehicle’s internal systems, they are less susceptible to data tampering and provide a secure flow of information directly to insurers. This security aspect reassures both insurers and consumers, fostering trust and encouraging adoption.

Continued innovations in OBD-II technology, which improve the granularity and accuracy of data collected, promise to sustain this segment’s market dominance. By offering insurers detailed insights into driving behaviors and vehicle usage patterns, OBD-II-Based UBI enables the development of highly personalized insurance policies that can adapt to the evolving needs of both insurers and their customers.

Vehicle Type Analysis

In 2023, the Passenger Vehicles segment held a dominant market position in the Usage-Based Insurance (UBI) market, capturing more than a 67% share. This predominance is primarily attributed to the high volume of passenger vehicles on the road compared to commercial vehicles, coupled with a growing consumer interest in personalized automotive insurance.

As individual car owners increasingly seek ways to reduce insurance costs in light of rising vehicle maintenance and ownership expenses, UBI provides a financially attractive solution by allowing premiums to reflect actual driving behavior and vehicle usage.

The surge in connected car technologies has further propelled the Passenger Vehicles segment. Most new passenger vehicles are now equipped with advanced telematics capabilities, making them ready platforms for UBI without the need for additional hardware installations. This technological integration simplifies the adoption process for consumers and insurers alike, enhancing the appeal of UBI programs.

Additionally, regulatory incentives for safer driving through technology-based insurance solutions have supported the growth of UBI in the passenger vehicle sector. Governments worldwide are encouraging policies that reward safe driving, aiming to reduce traffic incidents and promote road safety. This has led to an increased uptake of UBI products among everyday drivers who benefit from premium discounts for cautious driving behaviors.

Finally, the broad demographic appeal of UBI in passenger vehicles – from young drivers to the elderly – helps maintain its market dominance. Younger drivers, attracted by the potential for lower costs, and older generations, who appreciate premiums based on actual usage rather than statistical risk assessments, both find value in UBI. This wide appeal ensures continued growth and market penetration, reinforcing the strong position of the Passenger Vehicles segment in the UBI marketplace.

Key Market Segments

Type

- Pay-As-You-Drive (PAYD)

- Pay-How-You-Drive (PHYD)

- Manage-How-You-Drive (MHYD)

Technology

- OBD-II-Based UBI

- Smartphone-Based UBI

- Embedded Telematics-Based UBI

- Other Technologies

Vehicle Type

- Passenger Vehicles

- Commercial Vehicles

Driver

Growing Consumer Demand for Personalized Insurance Solutions

The Usage-Based Insurance (UBI) market is primarily driven by increasing consumer demand for personalized insurance solutions. As vehicle owners become more aware of the benefits of usage-based insurance, such as potential cost savings and rewards for safe driving habits, they are increasingly opting for UBI policies.

This demand is further supported by the rise in connected vehicles, which provide the necessary data to support UBI models. These connected vehicles facilitate the seamless collection and transmission of real-time driving data, enabling insurers to offer personalized rates and services that reflect the actual driving behavior of individuals. This trend is expected to continue growing as advancements in vehicle technology expand and become more sophisticated, promoting further adoption of UBI policies.

Restraint

Privacy Concerns and Data Security

Despite the growth, the UBI market faces significant restraints related to privacy concerns and data security. Many consumers are wary of sharing their personal driving data due to fears of how it might be used beyond calculating insurance premiums. The apprehension about potential breaches and misuse of sensitive information can deter vehicle owners from opting into UBI programs.

Insurers must navigate these concerns by enhancing data protection measures and being transparent about data usage policies. Establishing trust through rigorous security protocols and clear communication about data handling processes is crucial for wider acceptance and growth of the UBI market.

Opportunity

Integration with Emerging Technologies

The integration of UBI with emerging technologies presents substantial opportunities for growth within the industry. Advances in artificial intelligence (AI) and machine learning (ML) are particularly promising, as they can enhance the analysis of driving data and improve risk assessment models. Furthermore, the expansion of the Internet of Things (IoT) in automotive technologies provides additional touchpoints for data collection and customer engagement.

Insurers who leverage these technologies can develop more accurate pricing models and innovative insurance products, thus better meeting the needs of modern consumers. Additionally, the ongoing development of electric and autonomous vehicles represents a new frontier for UBI applications, potentially opening up new markets and customer segments.

Challenge

Regulatory and Compliance Issues

The UBI market also encounters challenges with regulatory and compliance issues across different regions. As UBI policies depend heavily on personal driving data, they are subject to varying legal frameworks regarding data protection and privacy that can differ significantly from one jurisdiction to another.

Insurers must carefully navigate these regulations to avoid legal pitfalls while also adapting their policies to comply with local laws. This regulatory environment can be complex and costly to manage, especially for insurers operating in multiple countries. Keeping up with evolving regulations and ensuring compliance is critical to avoid penalties and maintain consumer trust.

Growth Factors

The usage-based insurance (UBI) market is primarily driven by the rising popularity of connected vehicles and advancements in telematics technology. As more vehicles are equipped with built-in connectivity, the ease of implementing UBI programs increases, allowing for more accurate data collection on driving behaviors and vehicle usage.

This trend is further supported by consumer preferences shifting towards personalized insurance policies, where premiums are tailored to individual driving patterns, promoting savings and safer driving habits. The integration of technologies such as artificial intelligence and machine learning enhances the ability of insurers to analyze vast amounts of telematics data, refining risk assessment and pricing strategies to better match the actual risk profiles of drivers.

Emerging Trends

A key trend in the UBI market is the increasing use of smartphone-based telematics solutions, which utilize the widespread penetration of mobile devices to gather and transmit driving data without the need for additional hardware. This approach lowers barriers to entry for both insurers and consumers by utilizing technology that drivers already own and are familiar with.

Additionally, the expansion of electric vehicles (EVs) presents new opportunities for UBI, as these vehicles often come with advanced telematics systems that can provide detailed data on driving habits and vehicle health. As the automotive industry continues to evolve, UBI programs are also adapting to include features like real-time feedback to drivers and adaptive pricing models that reflect the dynamic nature of risk over time.

Business Benefits

For insurance companies, UBI offers substantial business benefits, including reduced claims costs and improved customer retention. By incentivizing safer driving behavior through potential premium discounts, insurers can decrease the likelihood and severity of claims. Furthermore, UBI programs provide insurers with a wealth of data that can be used to optimize pricing models and identify niche customer segments.

For consumers, the direct correlation between insurance costs and driving behavior can lead to significant cost savings, particularly for low-mileage and safe drivers. This personalized pricing model enhances customer satisfaction and loyalty, as policyholders appreciate the fairness and transparency of premiums that accurately reflect their individual risk.

Regional Analysis

In 2023, North America held a dominant market position in the Usage-Based Insurance (UBI) market, capturing more than a 40.5% share, with revenues reaching approximately USD 13 billion. This leading position can largely be attributed to the widespread adoption of telematics and connected car technologies across the region.

North American consumers have shown a robust interest in technology-driven solutions for vehicle safety and insurance, supported by the presence of major automotive and tech companies that continue to innovate in the telematics space. Moreover, the regulatory environment in North America has been conducive to the growth of UBI.

For insatance, in November 2023, Oyster launched the U.S.’s first usage-based rental insurance program, covering theft and damage for items like rental bikes, e-bikes, kayaks, and paddleboards. This expansion into the rental market marks a pivotal step for Oyster, aligning with the shift towards flexible, short-term insurance for recreational rentals.

The United States and Canada have implemented regulations that encourage the use of driving behavior as a basis for insurance pricing, which has been pivotal in fostering the growth of the UBI market. Insurers in these countries have been able to leverage extensive data analytics capabilities to offer competitive, behavior-based insurance products that appeal to cost-conscious and safety-oriented drivers.

In September 2023, Floow and Otonomo Technologies Ltd partnered with Definity and Munich Re to roll out a new usage-based insurance (UBI) product in Canada. This innovative collaboration uses telematics data to provide personalized auto insurance options, aiming to make premiums more reflective of individual driving behaviors. This partnership highlights the growing trend in Canada toward data-driven insurance solutions.

Additionally, the high level of urbanization and the increasing concerns about road safety in North American cities have driven consumer demand for UBI, as drivers look for ways to reduce insurance premiums through safer driving. The growing popularity of electric vehicles (EVs) in the region, which are often equipped with advanced telematics systems, also contributes to the expansion of UBI, providing insurers with detailed and accurate data on driving patterns and vehicle usage.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

The Key Players Analysis in the Usage-Based Insurance (UBI) Market typically focuses on leading companies driving market growth, innovation, and competitive strategies. In UBI, these players are notable for advancements in telematics, partnerships with tech providers, and customized insurance products tailored to consumer driving behaviors.

Allianz SE has been at the forefront of innovation in the UBI market. In recent years, Allianz has expanded its digital capabilities by acquiring several tech startups specializing in telematics and data analytics. These acquisitions have enabled Allianz to enhance its UBI offerings, providing more accurate and personalized insurance solutions to its customers. Additionally, Allianz has launched new products that integrate real-time driving data, rewarding safe drivers with lower premiums and promoting responsible driving behavior.

Progressive Corporation has also made significant strides in the UBI market. Known for its Snapshot program, Progressive has continuously improved its telematics-based insurance offerings. The company has invested in advanced data analytics and machine learning technologies to better assess driving behavior and offer customized insurance rates. Progressive’s commitment to innovation is evident in its recent product launches that cater to the evolving needs of modern drivers, emphasizing flexibility and personalization.

AXA has been proactive in expanding its presence in the UBI market through strategic partnerships and product development. The company has collaborated with various technology firms to integrate telematics into its insurance products, allowing for real-time monitoring of driving behavior. AXA’s focus on digital transformation has led to the introduction of new UBI products that offer customers greater control over their insurance premiums, aligning costs with actual usage and driving habits.

Top Key Players in the Market

- Progressive Corporation

- Allianz SE

- AXA Group

- Allstate Corporation

- State Farm

- Desjardins General Insurance

- Generali Group

- Liberty Mutual Insurance

- Insure The Box Limited

- UnipolSai Assicurazioni S.p.A.

- Aviva plc

- Zurich Insurance Group

- Other Key Players

Recent Developments

- October 2023: Allstate Corporation introduced improvements to its UBI program by integrating advanced telematics technology to better capture and assess driver behavior. This enhancement aims to provide more accurate, personalized premiums, aligning with the broader trend in the insurance industry of using technology to fine-tune risk assessments.

- November 2023: Progressive Corporation’s Snapshot program is gaining popularity, with drivers saving an average of $231 annually. Progressive’s strong presence in the UBI market underscores the appeal of data-driven pricing models, which offer incentives to customers who demonstrate safe driving habits.

- October 2023: AXA Group expanded its UBI offerings by launching a mobile app that enables customers to monitor their driving habits in real time. This app not only fosters customer engagement but also provides immediate feedback, encouraging safer driving practices and personalized policy adjustments.

- August 2023: Liberty Mutual Insurance teamed up with a tech startup to develop AI-based tools for analyzing driving patterns, which will enhance its UBI offerings. This partnership reflects Liberty Mutual’s strategic investment in technology to improve product offerings and further personalize insurance options.

- November 2023: Zurich Insurance Group initiated a pilot UBI program that leverages data from connected vehicles to tailor premiums based on actual driving habits. This program aims to enhance road safety and customer satisfaction by offering policies that closely align with individual driving behaviors, adding value through real-time, data-informed insights.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 32.1 Bn |

| Forecast Revenue (2033) | USD 299 Bn |

| CAGR (2024-2033) | 25% |

| Largest Market | North America |

| Base Year for Estimation | 2023 |

| Historic Period | 2019-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Pay-As-You-Drive (PAYD), Pay-How-You-Drive (PHYD), Manage-How-You-Drive (MHYD)), By Technology (OBD-II-Based UBI, Smartphone-Based UBI, Embedded Telematics-Based UBI, Other Technologies), By Vehicle Type (Passenger Vehicles, Commercial Vehicles) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Progressive Corporation, Allianz SE, AXA Group, Allstate Corporation, State Farm, Desjardins General Insurance, Generali Group, Liberty Mutual Insurance, Insure The Box Limited, UnipolSai Assicurazioni S.p.A., Aviva plc, Zurich Insurance Group, Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PD |